April 13, 2011 Daily Report, Howards' Hog Fund

2011-02-19 @ 08:12:42

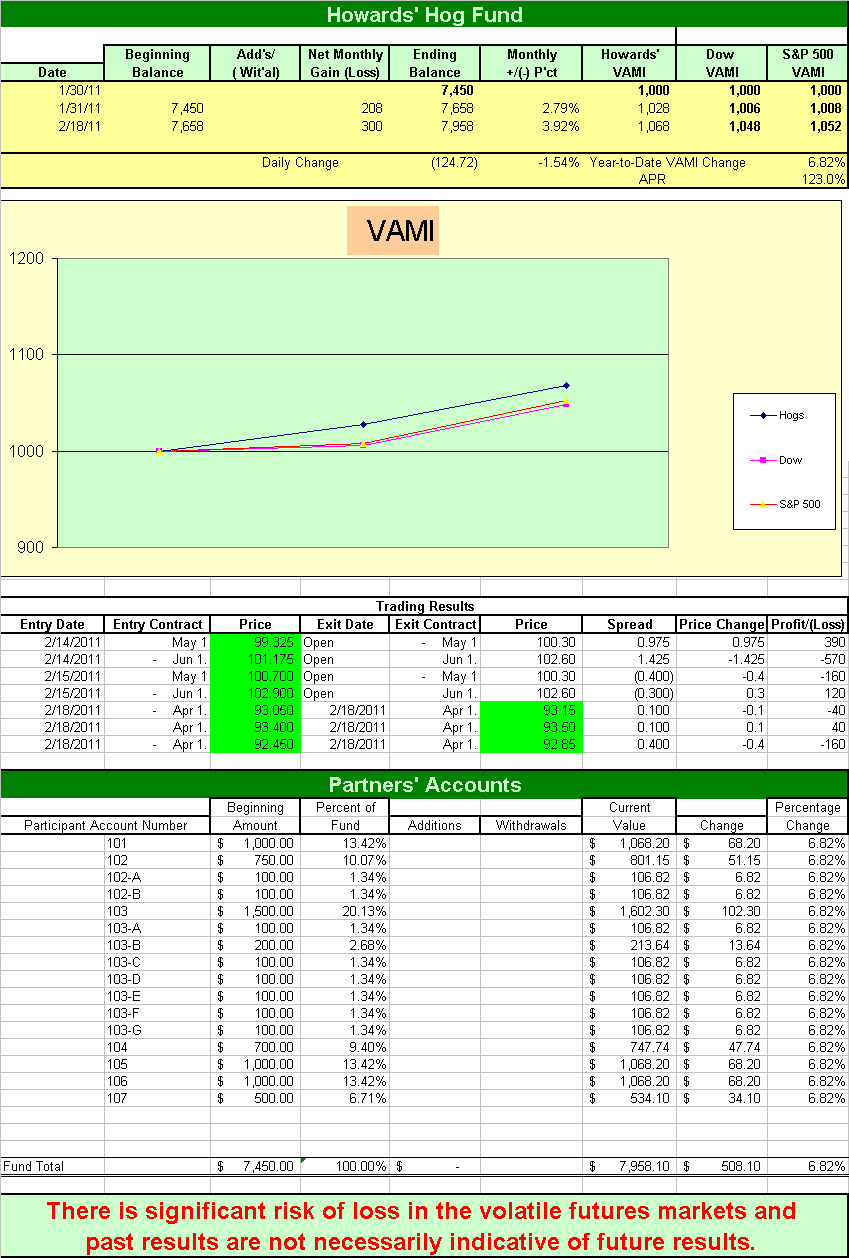

Howards' Hog Fund is performing very well as you can see in the table below.

Thanks for dropping by for a visit.

Best wishes,

dhm

Thanks for dropping by for a visit.

Best wishes,

dhm